Five More Thoughts On The Most Important Thing In Tech — FAMGA

Five More Thoughts On The Most Important Thing In Tech — FAMGA

On January 1st I published a Medium post titled “FAMGA (aka Facebook, Apple, Microsoft, Google, Amazon) Is Eating The World”. I thought it…

On January 1st I published a Medium post titled “FAMGA (aka Facebook, Apple, Microsoft, Google, Amazon) Is Eating The World”. I thought it was an important piece about the increasing dominance of the five leading tech companies. It turned out that other people didn’t think it was so important. After two months it had a paltry 400 views on Medium.

But I couldn’t stop thinking about the implications of the increasing dominance and the resulting implications of FAMGA. Every day I saw something that I thought was FAMGA related. So I fleshed out my first piece, and on April 9th I published “The Profound Implications of 5 Increasingly Dominant Tech Companies”. Two weeks later that post has 10,000 views. The piece struck a chord. You should read that before you read this.

The second FAMGA piece lead to a slew of interesting conversations and email threads. The highlight was my FAMGA discussion with the legendary investor Michael Steinhardt:

Hanging With Michael Steinhardt

In this (third) FAMGA piece, I’m going to highlight five of the the most interesting FAMGA related pieces I’ve read over the last 2 weeks that have helped me evolve and/or solidify my FAMGA thesis, which to review is:

The most valuable companies in the U.S. are increasingly tech companies.

The concentration of value (as denoted by market cap) being created in tech, is increasingly being created by the five largest companies, Facebook, Apple, Microsoft, Google and Amazon (aka FAMGA)

The concentration of market cap in just five hands will have an increasingly profound negative impact on innovation and it will increase wealth concentration (which is a major problem in the world today).

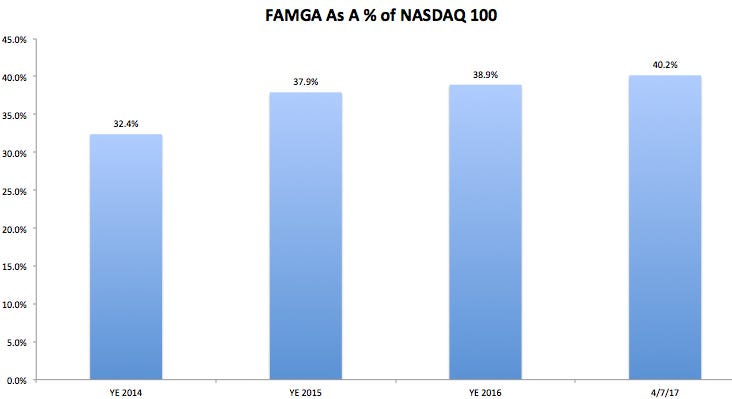

This graph illustrates FAMGA’s market cap/value concentration:

Below I highlight five FAMGA related posts.

1. Facebook and the Cost of Monopoly

Ben Thompson, Stratechery, April 19th, 2017

I didn’t know Ben Thompson before someone sent me this article. I’m now a Ben Thompson fanboy. This piece as a stand alone is quite dense. But to fully appreciate it, you need to read his past (dense) posts (e.g. Anti-Trust and Aggregation, The Audacity of Copying Well, Manifestos and Monopolies…) upon which this post is built.

In “Facebook and the Cost of Monopoly”, Ben writes what others have written about Facebook, that “By making Instagram Stories identical to Snapchat Stories, Facebook reduced the competition to who had the stronger network, and it worked”. But what Ben does that is truly thought provoking is, through a series of graphs, he illustrates how Facebook uses it’s monopoly position (as a driver of more than 40% of all traffic to the average news site) to capture almost all of the value that would otherwise accrue to the publishers or to the advertisers.

All this analysis brings Ben to the same place that I ended up, the belief that monopolies decreases innovation. Ben writes that “A monopoly, though, doesn’t need that drive to innovate — or, more accurately, doesn’t need to derive a profit from innovation, which leads to lazy spending and prioritizing tech demos over shipping products. After all, the monopoly can simply take others’ innovation and earn even more profit than they would otherwise”, and then he shares one more graph at the end of the piece to prove that point.

2. Why We’re Entering an Enterprise Tech Arms Race

John Frankel, ffVC, April 12th, 2017

In my last post I pointed out (as shown in a great chart from the Economist) that the history of tech has taught us that nothing is constant but change. But I finished by saying that “the forces compelling FAMGA to ever greater share of market cap are strong”. In this piece, John Frankel, a leading NYC based VC at ff Venture Capital, writes specifically about FAMGA “why this time is different”, which is a statement that is generally anathema to investors.

The main point John makes is that AI will help drive the enduring dominance of FAMGA as “…they have network effects — their products/services gain more value as more people use them — that are being extended and protected by AI. This will help them remain dominant for many years to come.” I think that’s a powerful observation.

3. The Firm of the Future

James Allen, James Root and Andrew Schwede, Bain & Co, April 12, 2017

There are several solid FAMGA related takeaways from this great piece, including that “Industries have become more winner-take-all. A Bain study of 315 global corporations found that just one or two players in each market earned (on average) 80% of the economic profit.”. It turns out it’s not just tech where the winners are dominating.

But Bain’s piece then highlights that tech companies, particularly FAMGA, have distinct advantages in terms of capital and human efficiency:

There’s other gold in the piece. Most notably, I was really intrigued by their insight that technology makes irrelevant the classic historic business tradeoff between scale and customer intimacy (for which Net Promoter Score is used as a proxy).

Bain’s piece gave me greater confidence in the enduring dominance of FAMGA.

4. Why Facebook Keeps Beating Every Rival: It’s the Network, of Course

Farhad Manjoo, New York Times, April 19th, 2017

The main point of Farhad’s article is that by copying Snapchat’s best features, and leveraging Facebook’s dominant network Facebook has “ ….. forced this coexistence. Facebook’s billions of users will now be introduced to Snapchat’s best features on Facebook’s own platform, eliminating, for a lot of them, any reason to switch. There is essentially no chance now that Snapchat will eclipse Facebook anytime soon, if ever. In other words, Mr. Zuckerberg has done it again; he has neutralized yet another rival”.

Now that’s the same point made by many others. The thing about this piece I found so interesting, was that Farhad shares my view of Facebook’s enduring dominance, but he ends up with the exact opposite conclusion. Farhad quotes Miranda Kerr, the fiancee of Snap CEO Evan Spiegel, commenting on Facebook’s copying of Snap features — “Can they not innovate? Do they have to steal all of my partner’s ideas? When you directly copy someone, that’s not innovation.” To which Farhad responds with “Meh. There are lots of different kinds of innovation in the tech industry. Coming up with something first is not the only kind of innovation”.

And Farhad is right about that. The graph below highlights three different types of innovation, and how the 1,000 largest corporations allocate their R&D budget between the three types and how they predict they’ll allocate R&D resources in 10 years:

The graph highlights that corporations spend less then 15% of their R&D budget on true breakthrough innovation. They spend the majority of their R&D budget on incremental innovation. Making existing products a little better (e.g. Pumpkin Flavored Oreos).

The point that I think Farhad misses is that Pumpkin Flavored Oreos doesn’t move the innovation needle for the world. And if dominant companies (like Facebook), with better algorithms, more data, and a bigger networks, can increasingly simply copy other people’s breakthrough innovation, capitalism will lead to less funding of true breakthrough innovation, because the returns are lower. While I agree that “Coming up with something first is not the only kind of innovation”, I think it’s the only kind of innovation that really matters.

5. 2017 YC Annual Letter

Sam Altman, YC, February 16th, 2017

Sam devotes less than 5% of the letter to a section on Hyperscale, which is his term for FAMGA, or as Sam describes the five behemoths, the winning “networked-effected technology companies”. Sam writes that these companies “…have powerful advantages that are still not fully understood by most founders and investors. I expect that they will continue to do a lot of things well, have significant data and computation advantages, be able to attract a large percentage of the most talented engineers, and aggressively buy companies that get off to promising starts. This trend is unlikely to reverse without antitrust action, and I suggest people carefully consider its implications for startups.”

That’s an ridiculously succinct statement of the FAMGA thesis.

Sam’s mention of “antitrust action” is obviously an issue to address in future FAMGA posts. “Is It Time to Break Up Google?” was a featured NYT editorial on April 22nd. . Notably, Ben Thompson wrote in “Antitrust and Aggregation” that “This monopoly, though, is a lot different than the monopolies of yesteryear: aggregators aren’t limiting consumer choice by controlling supply (like oil) or distribution (like railroads) or infrastructure (like telephone wires); rather, consumers are self-selecting onto the Aggregator’s platform because it’s a better experience. This has completely neutered U.S. antitrust law, which is based on whether or not there has been clear harm to the consumer (primarily through higher prices, but also decreased competition), and it’s why the FTC has declined to sue Google for questionable search practices”.

Sam finishes his letter on a very upbeat note “It’s an exciting time to do what we do.” I couldn’t agree with Sam more, but FAMGA remains an ominous overhang, the implications of which will be increasingly profound.

If you liked this post, please click the💚 below so other people will see it on Medium!

To sign up for my monthly newsletter with more articles like this click here