The ONE Stock Market Truth, & The TWO Potential Implications

The ONE Stock Market Truth, & The TWO Potential Implications

I was a stock market analyst in the 90s. My last four years were at Goldman Sachs.

I was a stock market analyst in the 90s. My last four years were at Goldman Sachs.

I don’t write about the stock market too often. I wrote this research report on Facebook in March of 2010. My 2014 revenue estimate was off by 1%.

I’ve written about FAMGA (my acronym for Facebook, Apple, Microsoft, Google & Amazon), and the implications of their dominance of tech market cap..

Last month I wrote “7 Reasons Why The Stock Market Is Going Up While The Economy’s Imploding.”

I think the stock market is really efficient. I don’t write about the market often, because it’s not often I think the market is mis-priced. But there’s some weird shit going on. And I have a pretty good idea what it is.

The One Stock Market Truth — We Are Paying MORE , For LESS

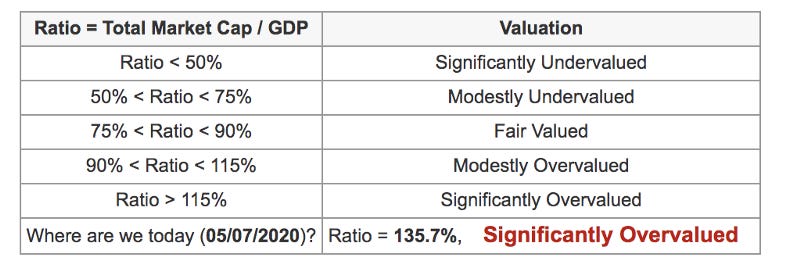

By more… I mean in terms of multiples. The one multiple I focus on is the Buffet Index. It’s simply the market cap of the stock market, over the GDP. It’s called the Buffet Index, because it’s Warren Buffet’s favorite macro indicator.

It’s currently 135, and we know GDP is coming way down. If we got todays numbers, I believe it would be at an all time high. It’s already eerily close. And it indicates the market is wildly overvalued relative to its long term trend.

By less, I mean in terms of growth. Take 3 yr, 5 yr, 10 yr gorwth, I beleive any of those outlooks should be at record lows for my lifetime. Before the pandemic, it was already expected to slow:

U.S. GDP growth will slow to 2.0% in 2020 from 2.2% in 2019. It will be 1.9% in 2021 and 1.8% in 2022. That’s according to the most recent forecast released at the Federal Open Market Committee meeting on December 11, 2019.2 The projected slowdown in was a side effect of the trade war. — The Balance

Things are obviously looking worse than that.

Way, way, way worse, IMHO.

So we are paying historically high multiples, for historically low growth.

So one of two things are going on.

1. This Time It’s Different

We’ve never had negative interest rates before. This is a truly strange and unique time. So maybe it is different. May it make sense to suspend everything we knew before, and recognize it’s a new world.

It’s possible that this time, it truly is different.

But I read “This Time Is Different: Eight Centuries of Financial Folly”, which chronicled the countless times weird financial things happened (e.g. the internet bubble), and the dominant response to “the market is wildly overvalued”, was to agree, or to state that “this time it’s different!”.

But for the last 800 years, it has not been different. For 800 years, there have been bubbles, and crashes, and pricing has been nonsensical for short periods of time. But for 800 years, strongest force in financial markets has been… reversion to the mean.

So it could different this time. But if it’s not, then ….

2. The Market Is Wildly Overvalued

If it’s not different this time. Then we’re paying historic high multiples, for historic low growth.

If it’s not different this time, at some point, in a week, or a year, or two, then reversion to the mean will insert itself in to reality, as it always does, and we’ll see an epic market collapse.

And it’s not more complicated than that.

I think it’s #2 above. That’s why I’m long Bitcoin. My viewpoint can be summed up by: “There’s A Massive Flood Of Fiat Coming, And Bitcoin Is Our Ark, So ….#GetOnTheBitcoinArk”. While I’ve long stated that Bitcoin does not need to be embraced by institutional investors to be a massive thing, it is nice when some of the most brilliant investors in the world embrace it as Paul Tudor Jones did on May 7, 2020 in this statement:

“I am not an advocate of Bitcoin ownership in isolation, but do recognize its potential in a period when we have the most unorthodox economic policies in modern history. So, we need to adapt our investment strategy. We have updated the Tudor BVI offering memoranda to disclose that we may trade Bitcoin futures for Tudor BVI. We have set the initial maximum exposure guideline for purchasing Bitcoin futures to a low single digit exposure percentage of Tudor BVI’s net assets, which seems prudent. We will review this exposure guideline regularly.” —

Thanks for clapping (up to 50 times)